European banks have made forward strides in managing climate and nature-related risks. But more still needs to be done as we often see that practices are only applied to a subset of relevant exposures, geographic areas and risk categories. To help banks improve further, later this year the ECB will publish an updated set of good practices observed in banks across Europe. European banks are well positioned to meet the prudential transition plan requirements, which the ECB will approach in a gradual and tailored manner.

European banks have made significant strides in addressing the risks stemming from the ongoing climate and nature crises. Considering that back in 2019 less than a quarter of euro area banks had reflected on how global heating and nature loss affected their own risk management, this is good news. Since then, banks have significantly stepped up their efforts. Now they have an increasing number of advanced practices in place to identify, monitor and – most importantly – manage climate-related and environmental risks.[1]

This progress has not come out of thin air. It has been achieved thanks to the hard work of many motivated bankers – including climate risk experts, risk managers and internal auditors – all across Europe in all types of banks, be they big, small, local or global. I would like to express my appreciation for these efforts. The progress made is also a testament to the effectiveness of the ECB’s multi-year strategy to ensure banks build up resilience to climate and nature-related risks.[2]

Walking the walk on climate and nature-related risks

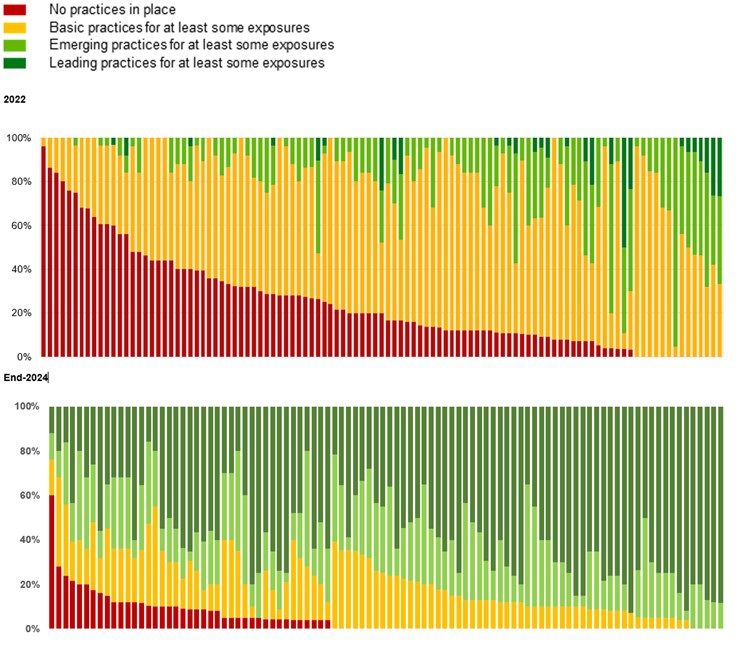

The evolution of banks’ climate-related and environmental risk management capabilities (Chart 1) shows that banks have walked the walk and made forward strides.

Chart 1

Banks’ alignment with ECB supervisory expectations on climate-related and environmental risks

Source: ECB

Notes: Chart shows level of maturity of individual banks’ practices aligned with 2022 C&E risks thematic review assessment grid. For consistency purposes, progress is measured against what was basic, emerging and leading practices in 2022. Outcomes focus on soundness of banks’ practices and do not represent the comprehensiveness of practices across all exposures.

This means, for example that a bank is ranked dark green if it has a leading practice in place, even if that leading practice only relates to a subset of its exposures. The same holds true for light green: this qualification indicates that a bank has emerging practices in place, even if that emerging practice only relates to a subset of its exposures. In other words, the charts do not say anything about the percentage of assets covered by leading or emerging practices.

In 2022, 25% of banks had no practices in place, 54% had basic practices for at least some exposures in place, 18% had emerging practices for at least some exposures in place and 3% had leading practices for at least some exposures in place.

By the end of 2024, 5% of banks had no practices in place, 17% had basic practices for at least some exposures in place, 22% emerging practices for at least some exposures in place and 56% leading practices for at least some exposures in place.

Yet it is also fair to say that the journey has not always been easy. Back in 2022, almost 80% of banks had either only basic climate-related and environmental risk management practices in place or none at all. Based on their modest levels of preparedness at the time, after the 2022 thematic review on climate-related and environmental risks and the climate risk stress test, we encouraged banks to speed up their progress and we set clear interim deadlines for 2023 and final deadlines for the end of 2024.

Let me be clear: on a positive note, the number of banks lacking foundational elements has decreased sharply in the last few years.[3]

For our first interim deadline in March 2023, by when banks had been asked to have a sound materiality assessment in place[4], the ECB issued 28 binding decisions on strengthening internal risk management to start properly considering climate-related and environmental risks, 22 of which involved the potential imposition of periodic penalty payments (PPPs) if banks failed to meet the requirements set out in these decisions. For the small number of cases where banks might have lacked these foundational elements after the deadline in these decisions had passed, the process to determine whether periodic penalty payments have accrued is currently ongoing. We will communicate more details at the end of this process.

For the second interim deadline set at the end of 2023 concerning the integration of C&E risk into banks’ governance, strategy and risk management, most banks have made notable strides. Therefore, only nine outlier banks that did not have the foundational elements in place to adequately manage these risks by the time of the deadline, received binding supervisory decisions, including the potential imposition of PPPs should the banks fail to comply with the requirements. Some of the deadlines set in these decisions still have to come due and, where they have already come due, the process to determine whether PPPs have accrued is ongoing.

With regard to our final deadline at the end of 2024, by when banks were asked to include climate-related and environmental risks in their stress testing and internal capital adequacy assessment processes (ICAAPs), we are finalising our assessment and already see that the number of banks not meeting the foundational elements has decreased even further.

Encouragingly, we see not only the foundational weaknesses decreasing but also the set of sound and advanced practices growing. For example, banks’ materiality assessments are becoming increasingly sophisticated and show that the external reality is better reflected in banks’ understanding of the risks they face. This has led to more than 90% of banks currently considering themselves to be materially exposed to climate-related and environmental risks. That is significantly higher than in 2021, when only half of banks reached this conclusion.

While we can see that banks’ practices have become more robust over time, they should serve as a basis for self-sustained progress in the banking sector to apply these sound practices more comprehensively. For example, we often see that banks’ sound practices are only applied to a subset but not all relevant exposures, risk categories and geographical areas. In the context of collateral valuation, for example, we see that banks may only apply these practices to transition risks but not physical risks. Moreover, banks are having difficulties in covering all their important portfolios. For example, mortgage lending – a sizeable part of European banks’ business – is not always fully considered in banks’ strategy to manage climate and nature-related risks. In addition, banks are more advanced in covering climate and nature-related risks in credit risk, but less so in other risk categories, such as operational risk or market risk. Moreover, banks are also struggling with concrete risk quantification in certain areas.

That’s why our supervisory teams will continue tracking progress and urging banks to make sure they roll out their sound practices across all material portfolios, geographical areas and risk categories, covering both climate and nature-related physical and transition risks.

Inclusion in stress testing and capital adequacy assessment

Stress testing is one key tool to better quantify where climate and nature-related risks lie in a forward-looking manner. Importantly, climate risk stress testing is still the most frequently observed tool used to quantify capital as part of banks’ ICAAPs. Moreover, banks use the findings from stress testing physical risks, for example, to prioritise data collection for risk management within precise geographical areas where the highest risks lie. In addition, stress testing can help banks tailor their strategic positioning to a changing economy, but crucially without having to abandon sectors in which they have built up expertise.

On a positive note, all banks have now included climate risk in their stress testing framework. That is great progress compared with 2022, when only 41% of banks had done so.

Still there is more work to be done to make sure stress testing frameworks are fully comprehensive. For instance, not all banks have included all material risk drivers, relevant portfolios or transmission channels. This suggests that some may still be underestimated. What’s more, not all banks have included nature-related risks in their stress testing frameworks, which is concerning given that the decline in ecosystem services is a material source of financial risks.[5]

Moreover, three-quarters of banks do not yet cover all material climate and nature-related risk drivers in their ICAAPs, which also indicates that risks may be underestimated. So far, only one-third of banks explicitly integrate climate-related risks into their capital plans. Looking ahead, banks must make their ICAAPs more comprehensive to ensure their capitalisation is commensurate with the underlying risk.

The increasing materiality of climate and nature-related risks

Climate and nature-related risks are already a reality, and the materiality of these risks is clearly rising.[6] And thus banks also need to make further improvements in their preparedness.

Global heating is already on the cusp of crossing the 1.5 degrees Celsius threshold. Regrettably, the world is on track for an average temperature increase of 3.1 degrees Celsius by the end of the century. And even that depends on all governments sticking with their current policies and implementing them on time and in full.[7]

The physical risks that are already materialising ‒ the floods in Valencia last year, the heatwave that swept across Europe last week[8] or the forest fires that risk turning into urban fires and have been threatening the outskirts of Marseille this week ‒ are just the tip of the iceberg. Imagine a world subject to 3.1 degrees Celsius of global heating…

Scientists – and increasingly also financial market participants – are sounding the alarm. The insurer Allianz, for instance, has warned that global temperatures are fast approaching levels where insurers would no longer be able to operate, creating “a systemic risk that threatens the very foundation of the financial sector”.[9] And Swiss Re’s latest “sigma” report identifies a long-term trend of a 5-7% annual increase in insured losses from natural catastrophes, suggesting that these losses will simply continue to rise.[10] Others highlight that, unlike cyclical risk drivers, climate risk is a permanent shock heading in only one direction, with serious long-term effects on house prices and other asset values.[11]

That’s why continuously updating materiality assessments is crucial. As our models improve and more data become available, estimates of the economic impact of the climate and nature crises are consistently being revised upwards.[12] Moreover, we know that the methodologies and scenarios underpinning these assessments likely result in risks being underestimated. For instance, when it comes to physical risks – such as floods, heatwaves or wild and urban fires – experts warn that they may be severely underestimated, particularly because the models do not account for tipping points or compounding events. The climate crisis is unfolding faster than previously assumed, with impacts materialising at lower than estimated temperatures.[13]

The ECB will therefore continue to monitor developments in banks’ materiality assessments, because they are key to effectively identifying the forward-looking risks that banks need to focus on.

The importance of good data to identify risks and opportunities

The availability of reliable, meaningful and comparable data from companies remains essential to know where the risks are hiding and where opportunities can be found. In this context, the reporting requirements in the EU’s sustainable finance framework are providing indispensable information about financial risks and are a solution to the patchwork of different reporting criteria.

When discussing simplification initiatives striking the right balance between how much data firms report and how many firms are required to do so is therefore crucial. While it is important to preserve vital data to assess climate and nature-related financial risks and opportunities, there is room to simplify and reduce reporting requirements. However, excluding too many firms from the Corporate Sustainability Reporting Directive could reduce the availability of information about important parts of our economy. This is why our ECB opinion proposed – in addition to the European Commission’s threshold of 1,000 employees – also including medium-large undertakings (with 500-1,000 employees) that would report under simplified and more proportionate reporting standards.[14]

A pragmatic and targeted approach to transition planning

Considering the notable progress in managing C&E risks, banks under European supervision are well positioned to meet the forthcoming prudential transition planning requirements that will come into effect in 2026.[15]

The ECB will approach transition planning requirements in a gradual and targeted way, focusing on new elements in the European Banking Authority’s Guidelines on the management of environmental, social and governance risks. This is because most of the provisions in these Guidelines have already featured in our supervisory assessments to date. Where there are persistent shortcomings, such as on comprehensiveness and coverage of portfolios and geographic areas, Joint Supervisory Teams will discuss these with the banks as part of their regular supervision. As a first step as part of our prudential transition planning mandate, at the end of this year and throughout 2026 we will start informal dialogues with the banks to discuss progress, challenges and areas for improvement. Only at a later stage, in 2027, will we carry out a more formal assessment.

Next steps

One way of improving preparedness is to draw on the good practices that we have already seen in banks across Europe. After all, our unique perspective as European supervisor enables us to benchmark practices across Europe. Building on the positive response to our earlier good practices reports from climate stress test and the thematic review, later this year we will publish an updated compendium of good practices that banks of different sizes and business models from different countries will be able to draw on. Moreover, we will host an industry outreach conference on 1 October 2025, where we will discuss progress, good practices and the remaining challenges in risk management and capital planning.

European banking supervision will continue to strive for a European banking sector that is resilient to all of the material risk drivers they face, including those stemming from the climate and nature crises. Because only resilient banks can play their vitally important role in the economy, financing much-needed investments in the green, digital and defence transitions so that we can preserve our way of life and remain masters of our own destiny.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

In European banking supervision we have typically referred to climate-related and environmental risks, or C&E risks. For the purposes of this blog post, I will consider the terms “environmental risks” and “nature-related risks” as interchangeable.

The ECB first started discussing C&E risks with banks back in 2019, when less than a quarter of banks had demonstrably reflected on how the climate and nature crises affected their risk management. In 2020 the ECB published a guide setting out its understanding of the sound management of C&E risks under the existing prudential framework. In subsequent years we conducted several in-depth supervisory exercises, including a bank self-assessment exercise in 2021, and a thematic review on C&E risks and a climate risk stress test in 2022. We then set clear interim and final deadlines by which banks had to meet certain conditions to be able to manage their C&E risks.

For more information on the interim and final deadlines, see Elderson, F. (2024), “Sustainable finance; from “eureka!” to action”, speech at the Sustainable Finance Lab Symposium on Finance in Transition, Amsterdam, 4 October; and ECB (2025), “Material exposures to physical and transition risk drivers of climate change”, ECB Annual Report on supervisory activities 2024.

For more information on the importance of materiality assessments for banks to be able to manage risks, see Elderson, F. (2024), “You have to know your risks to manage them – banks’ materiality assessments as a crucial precondition for managing climate and environmental risks”, The Supervision Blog, ECB, 8 May.

See Elderson, F. (2025), “Nature’s bell tolls for thee, economy!”, speech at the Naturalis Biodiversity Center, Leiden, 22 May, and Ceglar, A., Danieli, F., Heemskerk, I., Jwaideh, M. and Ranger, N. (2025), “The European economy is not drought-proof”, The ECB Blog, 23 May. Surface water scarcity alone puts almost 15% of the euro area’s economic output at risk.

Already in the next five years, extreme weather events could put at risk up to 5% of euro area economic output, the NGFS short term climate scenarios find. See Mauderer, S. and Stracca, L. (2025), ‘’Climate risks: no longer the tragedy of the horizon’’, The ECB blog, 9 July.

United Nations Environment Programme (2024), Emissions Gap Report 2024, 24 October. It is difficult to overstate how catastrophic this warming would be. Each fraction of warming leads to an uptick in the severity and frequency of dangerous heatwaves, storms, wildfires and other disasters. Scientists say that 3 degrees Celsius could lead to the collapse of numerous ecosystems, months-long heatwaves, widespread drought and crop failure, mass coral bleaching, rapid ice sheet melting and other potentially irreversible events.

Allianz estimates that GDP losses from heatwaves range from -0.1 percentage points for Germany to as much as -1.4 percentage points for Spain, with total losses of -0.5 percentage points for Europe, -0.6 percentage points for the United States and -1.0 percentage points for China. To put this into perspective, one day of extreme heat (above 32 degrees Celsius) is equivalent to half a day of strikes. See Allianz (2025), “Global boiling – Heatwave may cost -0.5pp of GDP in Europe”, 1 July.

Thallinger, G. (2025), “Climate, Risk, Insurance: The Future of Capitalism”, 25 March.

Swiss Re Institute (2025), Natural catastrophes: insured losses on trend to USD 145 billion in 2025, sigma report, 29 April.

Clark, P. (2025), “How the next financial crisis starts”, Financial Times, 26 June.

For example, according to the latest estimates from the Network for Greening the Financial System, the potential loss of global GDP if climate action falters is now projected to be three times higher than in earlier assessments from just a few years ago. See Aerts, S., Stracca, L. and Trzcinska, A. (2024), “Economic losses from climate change are probably larger than you think: New NGFS scenarios”, VoxEU Column, Centre for Economic Policy Research, 22 October.

Trust, S. et al. (2025), Planetary Solvency – finding our balance with nature, Institute and Faculty of Actuaries, January.

The revised Capital Requirements Directive (CRD VI) includes a new legal requirement for banks to prepare prudential plans to address climate-related and environmental risks arising from the process of adjustment towards climate neutrality by 2050. CRD VI mandates supervisors to check these plans and assess banks’ progress in addressing these risks.